By Geoff Allan, Managing Director at Partners for Growth

LAVCA’s (The Association for Private Credit Investment in Latin America) annual global get-together in New York for LATAM-based founders, early and late-stage investors, and limited partners wrapped up with another successful event in October. PFG had the pleasure of attending – as an opportunity for folks in the larger Latam tech ecosystem to connect, trade ideas and war stories, and cement new partnerships. The annual summit continues to bring together many of the most compelling voices across Latam’s tech and startup community.

It’s no surprise that the last year was a period of evolution/readjustment across the tech landscape in LATAM. The region has not been immune to the rising global interest rates, pullback in capital across stages, and a more subdued acquisition environment. Founders and boards continue to adapt to these headwinds.

However, a singular theme running through all our discussions was that the structural growth of tech across LATAM continues and is accelerating. How can that be, given the headwinds above?

In light of the current environment, we wanted to highlight some main themes discussed with founders and funders. While these are not unique to PFG as a growth capital/debt fund, we wanted to underscore five themes coming out of LAVCA of why PFG remains excited about the long-term opportunities in LATAM.

Demographics

The greater LATAM region remains an enormous – and relatively speaking untapped – market for a variety of consumer, SMB, and enterprise applications. As home to roughly 650 million people, LATAM is almost twice the size of the US and not quite twice the EU in population. It’s similar in size to the overall MENA region (with less oil export concentration) and a population skewing younger generally vs. the US and EU. GDP per capita has continued to increase over the last decade and is on par with some of the more developed regions of SE Asia.

Unit Economics

The impact of higher interest rates, falling tech equity valuations in public and private markets, and a stricter capital environment – across the board, but especially for companies in the later stage/growth equity space – has forced most LATAM tech companies to reevaluate their business models. The growth vs. burn calculus has changed. Putting aside some of the few exceptional companies with exceptional teams and metrics, unprofitable companies continue to work on reducing burn and discretionary spending, improving margin profiles, and putting focus on lower but more efficient growth vs. go-for-broke plans. Companies that are already profitable/breakeven are positioning themselves for solid growth plans, product expansions aiming to grow market share, and selective acquisitions.

Capital

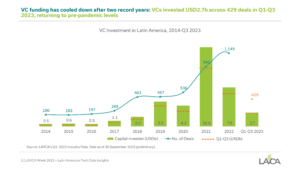

It’s no secret capital flows have reduced markedly over the last 18 months, and LATAM has seen that as well. After an explosion of roughly 4x growth to $16 billion in venture capital invested in LATAM in 2021, flows fell significantly in 2022 and 2023 to approximately $1 billion per quarter and $1.7 billion in the first half of 2023 (according to Q3 2023, LAVCA industry data), or ~$4 billion per year. However, while that represents a considerable contraction year-on-year, in overall terms, these levels are on par with annual levels seen as recently as 2019/2020 and still a 2x or greater increase from levels in the decade before 2019, thus representing continued steady growth (if removing the recent outlier period). Many participants acknowledged valuations and funding reached excessive levels over the past boom period. Private valuations of 20x or more revenue two years ago have fallen to 3-4x. The days of unlimited capital for companies seem behind us. But while the dynamics of readjusted valuations and/or down rounds will continue to shake out, the structural opportunity remains. For instance, venture investment in LATAM is still only ~0.1% of GDP, which is among the lowest in the world and less than 10x levels in the US and EU, and <5x India. LAVCA Public overall Latam tech valuations are <1.8% of GDP, vs. 3% in Brazil, 11% in India, 20% in China, and ~64% in the US (again, according Q3 2023, LAVCA industry data). While we can quibble with the specifics, the potential remains for hundreds of billions, if not trillions, of value to be created over the next one to two decades.

Ambition

The size and sophistication of LATAM tech continues to increase. One of the themes we have seen with founders is the expanding reach and capabilities of operations outside their home markets. Earlier criticisms (often from investors outside LATAM) worried local companies were growing to solve LATAM-specific problems with limited potential outcomes. However, companies are expanding to create models applicable to LATAM locales outside not only their home countries but with a level of robustness and originality born out of local conditions that make them exportable to other growth markets. Much of the work being done in fintech, healthtech, proptech, logistics, and marketplaces draws on solutions for underserved populations and are being built to tackle local complexities. Developing businesses in these challenging areas puts companies in a position to expand outside their home countries.

Resilience

One factor in our LAVCA conversations was the continued energy and optimism of founders – more challenging capital conditions notwithstanding – and the likelihood for large, cross-continental LATAM businesses to be created. LATAM entrepreneurs are used to having to do more with less – whether by choice or necessity. This is born out by recent surveys of LATAM tech CEOs, showing optimism has materially increased in 2023 vs. 2022, and almost two-thirds of LATAM polled companies are now hiring, compared to the majority of companies that were either flat or reducing headcount in 2022. No one is slowing down, and the overall trends continue.

In conclusion, LAVCA’s annual summit showcased the resilience and potential of the LATAM tech ecosystem, revealing an environment ripe for growth and innovation. Despite global economic challenges, the region’s favorable demographics, strategic recalibration of business models, and unwavering entrepreneurial spirit underline its promising trajectory. This paints a compelling picture for continued investment and development in Latin America’s tech landscape.

—

The views expressed are my own and do not necessarily reflect those of my employer.

This content is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. Any such offer will be made only to qualified investors through confidential offering documents. All investments involve risk, including the possible loss of principal. Past performance is not indicative of future results.